India has firmly established itself as a global hotspot for Global Capability Centres (GCCs), with over 1,700 unique entities supporting everything from transactional processes to cutting-edge innovation. These centers span 22 industries—ranging from BFSI and High-Tech to niche sectors such as aerospace, automotive, and education—and have matured significantly over the past decade.

From this broader landscape, we narrowed our scope to 1,368 GCCs aligned with six high-relevance verticals: Banking & Financial Services, Insurance, High-Tech, Healthcare & Life Sciences, Manufacturing, and Retail & CPG. This refinement was based on alignment with enterprise digital priorities, scale, and operational maturity. An additional filter removed 274 centers focused exclusively on core Engineering or R&D—functions that tend to fall outside the scope of enterprise transformation. The result: a focused universe of 1,094 GCCs best positioned for strategic engagement

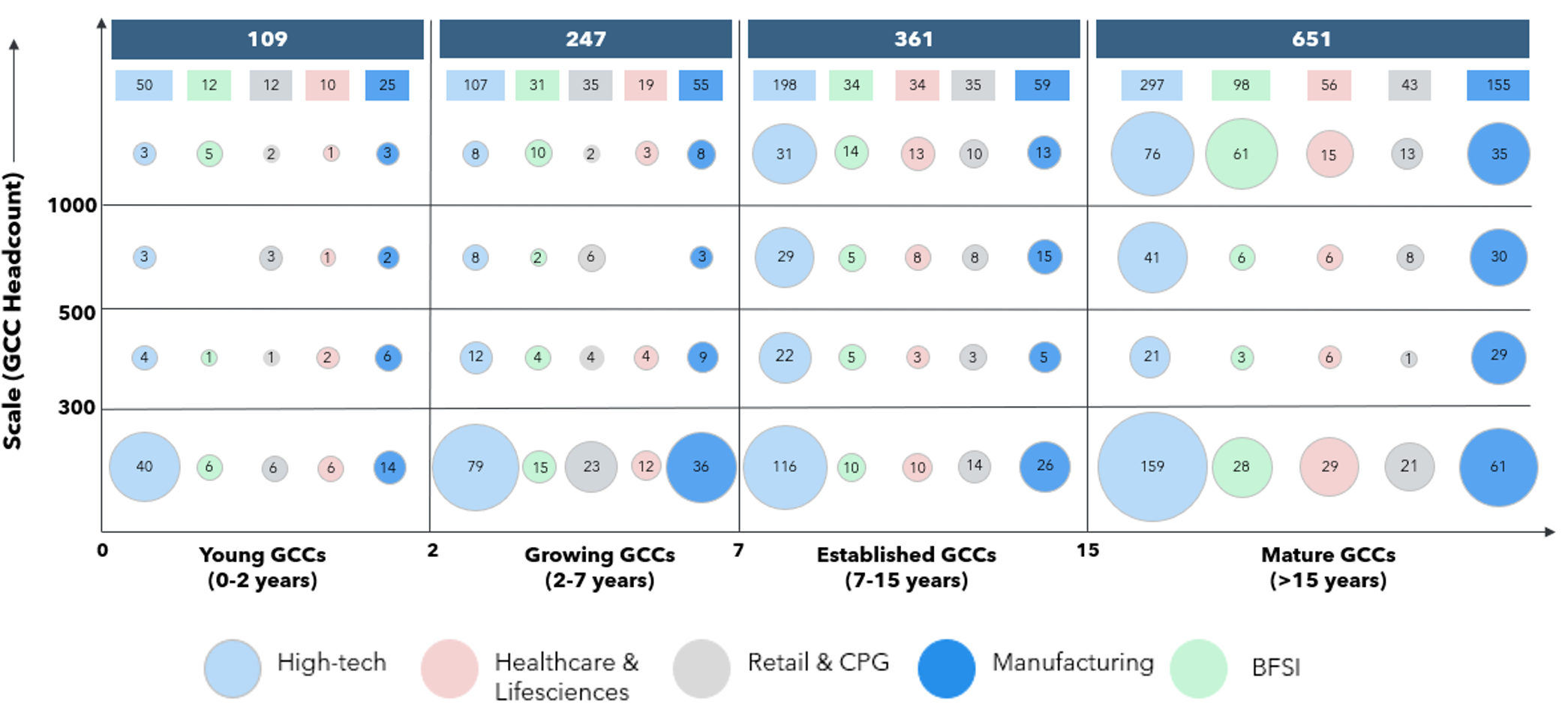

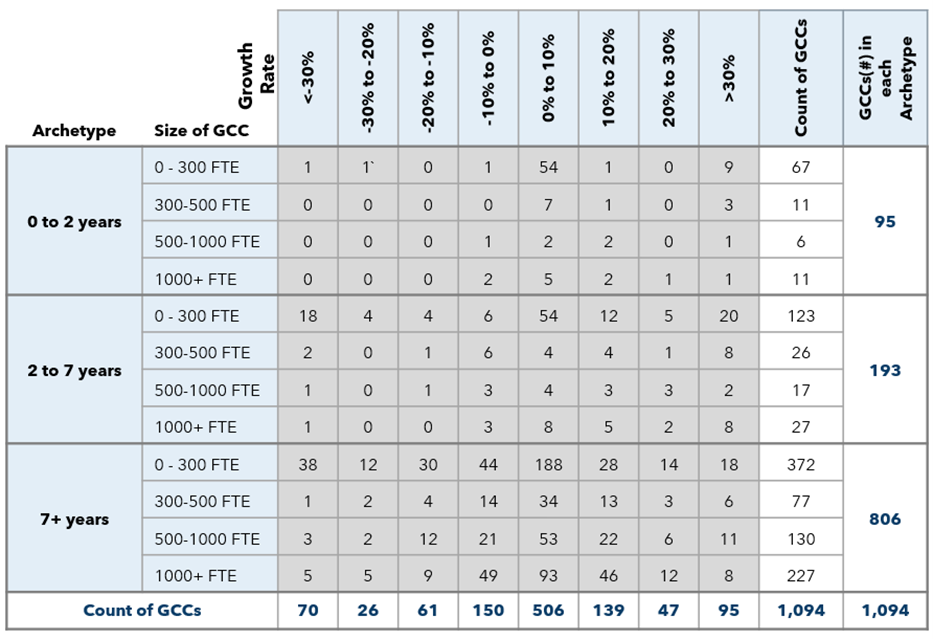

A closer look at the 1,094 prioritized GCCs reveals compelling patterns. Nearly 60% of these centers have been in operation more than seven years, underscoring their operational maturity—but also highlighting a growing need for reinvention and value re-alignment. In fact, more than 650 GCCs have crossed the 15-year threshold, forming a sizable legacy base now facing pressure to transform or monetize.

Banking and Financial Services, in particular, shows deep institutionalization, with over 35 GCCs surpassing the 1,000 FTE mark. These centers have become embedded engines for risk management, regulatory reporting, compliance, and digital acceleration. High-Tech, on the other hand, is marked by a younger, mid-scale profile. While many of these centers are scaling rapidly with digital-first charters, others are struggling to evolve—creating a clear bifurcation between transformation hubs and stagnating candidates.

In Healthcare & Life Sciences, around 15% of GCCs have scaled beyond 1,000 FTEs. Industry leaders like GlaxoSmithKline and Providence are using their India-based centers to lead R&D, digital regulatory operations, and real-world evidence generation. Retail & CPG, though a smaller cluster in terms of absolute numbers, has seen concentrated growth. About 42% of mature GCCs in this vertical have undergone transformational expansion—driven by firms like Ferrero and Bunge, who are doubling down on analytics, supply chain intelligence, and eCommerce enablement.

Meanwhile, Manufacturing GCCs, while typically smaller, are quietly emerging as innovation hubs. Sixty percent of recent setups operate with under 300 FTEs, yet 20% have scaled beyond 500 FTEs. Notable examples include EagleBurgmann and DuPont, both of whom are using their GCCs to drive digital engineering, automation, and operational excellence.

A sharp divergence is emerging across verticals.

In High-Tech, which includes 495 mature centers, we observed a “two-speed” market. On one end, over 140 GCCs have expanded headcount by more than 20% in the last two years—many taking on roles in AI, cloud, cybersecurity, and analytics. On the other, about 18 centers have seen declines of over 20%, signaling potential candidates for restructuring, cost optimization, or divestiture.

Banking & Financial Services comprises over 160 centers, with nearly one-third now operating at a scale greater than 1,000 FTEs. These GCCs are not just service arms—they are leading KYC automation, real-time compliance analytics, and even GenAI-enabled customer engagement pilots. In parallel, Insurance has over 75 centers, and more than 20% have crossed the 1,000 FTE mark. Their strength lies in claims management, underwriting analytics, and fraud detection—areas now ripe for AI augmentation.

In HLS, 63% of GCCs remain relatively small (<300 FTEs), but 15% have grown beyond 1,000 FTEs. What’s even more telling: nearly 90% of new centers were established within the last two years, largely by global pharma and medtech firms investing in AI-led R&D and digital regulatory infrastructure.

Manufacturing GCCs, while still compact, are evolving. Over half are under 300 FTEs, but a rising 20% have scaled past 500 FTEs. Meanwhile, about 27 mature GCCs with limited growth trajectories are now in the spotlight as potential carve-outs or JV candidates.

Retail & CPG has emerged as a fast-evolving cluster, with 60% of young GCCs (established within the last 5 years) launched by US-based firms. Roughly 42% of mature GCCs in this space have pivoted towards analytics-driven supply chain orchestration and e-commerce enablement.

Traditional captive structures are giving way to dynamic, hybrid models. Increasingly, firms are blending internal GCC teams with third-party partners—especially for digital and AI-first programs. Build-Operate-Transfer (BOT) structures are accelerating time-to-scale, while virtual GCCs are enabling asset-light expansion in functions like cybersecurity, GenAI research, and global finance.

This architectural flexibility is being complemented by commercial innovation. Gainshare and outcome-based contracts are replacing headcount-linked billing models. Subscription-based delivery is gaining traction, particularly for compliance, HR, and modular digital operations. This shift reflects a deeper desire across enterprises: to unlock innovation at scale without losing execution control.

Yet, this momentum is not without friction. Talent scarcity—especially for digital and GenAI capabilities—remains a concern, with attrition pressures continuing in metro markets. Geopolitical uncertainty is also prompting diversification, with increased interest in Tier-2 cities and dual-country footprints.

Hybrid delivery models, while flexible, introduce governance complexity. Enterprises often struggle to maintain culture, cohesion, and compliance across fragmented delivery setups. Further, GCCs eyeing divestiture often lack the modularity, documentation, and governance required for smooth transitions.

For service providers, this is a pivotal moment. There are two clear plays:

First, enabling high-growth GCCs to scale further—through digital platform buildouts, innovation pods, and managed transformation programs. Providers who can deliver outcome-based models and accelerate talent ramp-up will be vital partners.

Second, partnering with enterprises seeking to realign, monetize, or divest aging GCCs. This includes delivering operational assessments, leading carve-out planning, and even running BOT transitions.

Two case examples illustrate this:

India’s GCC ecosystem is entering its next phase—defined not by scale alone, but by strategic direction. Some enterprises are investing aggressively to make their centres innovation engines; others are pulling back, rethinking operating models, or monetizing legacy assets.

What’s clear is this: The age of passive GCC management is over.

Enterprises must regularly reassess the role, structure, and strategic value of their GCCs. And service providers that understand the nuance of growth vs. exit decisions—offering bespoke support in both trajectories—will shape the future of global delivery.

By Abhisek Srichandan, Associate Consultant