In recent years, Europe has been hit by a pandemic, double-digit inflation, and a war. The subsequent supply chain disruptions, shortages of food and fuel, and looming recession do not make anything any easier for IT organizations on the continent. Still, IT budgets are rising. Not necessarily at the pace of rampant inflation. But still more than typical in times of economic contraction. It is starting to become clear that most enterprises now view IT as a strategic resource in weathering uncertainty. IT is no longer seen as a cost center but as a strategic resource that can impact the top and bottom lines.

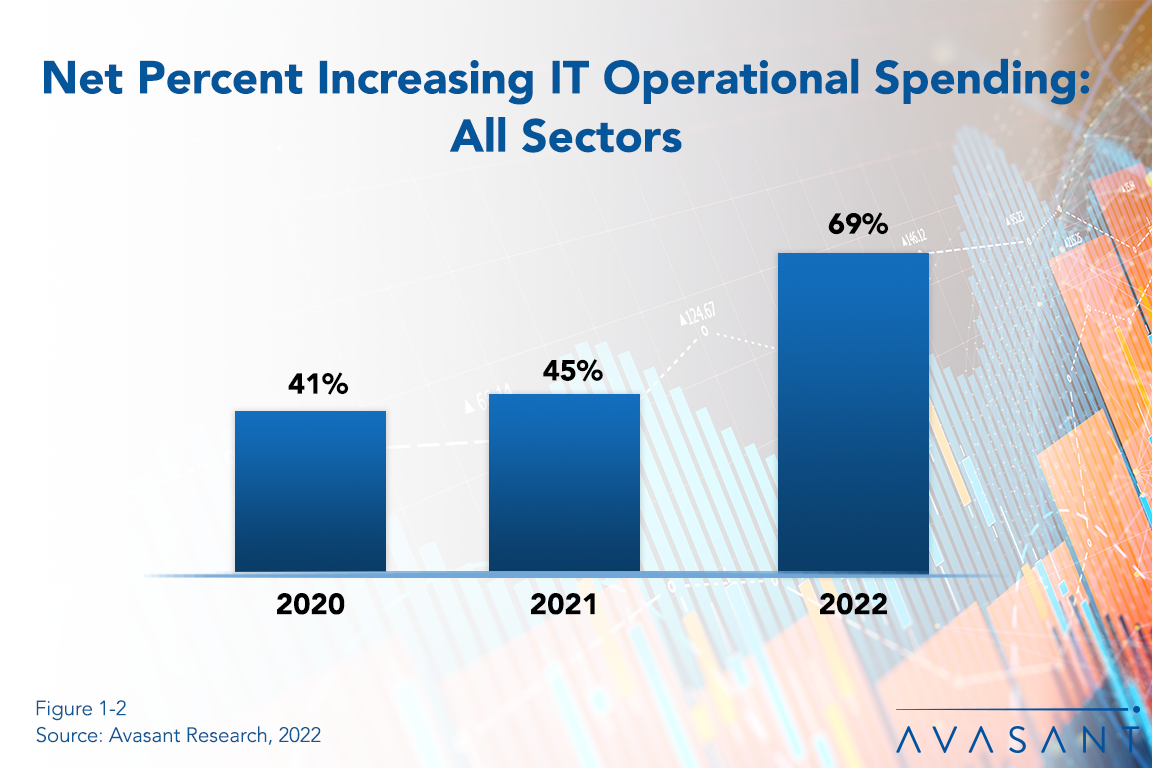

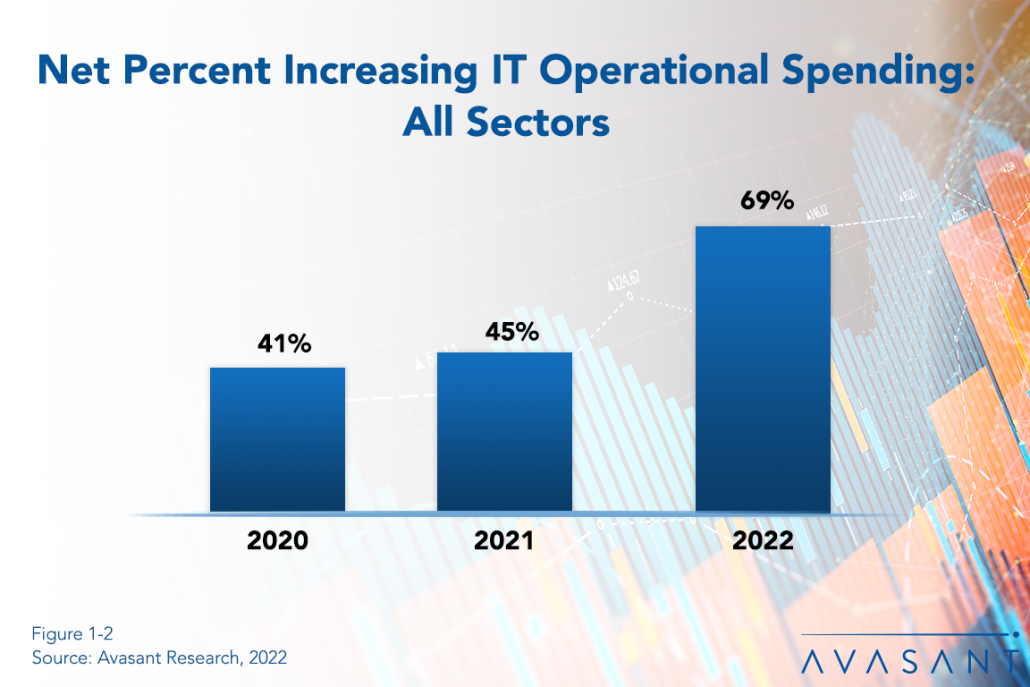

As shown in Figure 1-2 from the free executive summary of our European IT Spending and Staffing Benchmarks 2022/2023 study, more companies are planning IT budget increases than at any time in the cloud era, with a net 69% increasing spending. About 79% of companies are planning IT operational budget increases, with only 10% planning budget cuts. At the median, companies are projecting 4.5% IT budget increases, also the biggest we have seen in the three years we’ve done a European-focused study.

The European IT department of the present is more resilient, flexible, innovative, and focused on the business than even just a couple of years ago. Around 39% of European companies report that they now have at least half of their applications in the cloud, up from 24% in 2020. Cloud infrastructure has gone from an average of 4.6% of the total IT operational budget last year to 6.5% this year. Data analytics, digital transformation, and systems and data integration follow right behind cloud apps and cloud infrastructure as top categories of new spending initiatives.

One sign of innovation is the declining percentage of an IT budget spent to merely “keep the lights on.” We began tracking that number for European companies just last year, and, at the median, companies spent 70% of IT budgets on running the business and the other 30% on either growing or transforming the business. This year, at the median, the percentage of the budget spent on running the existing business is only 60%. A full 20% is dedicated to transforming the business compared with 13% last year.

“The proximity to the war in Ukraine has naturally made European companies a little more cautious than their counterparts in the US and Canada,” said David Wagner, senior research director at Computer Economics, a service of Avasant Research, based in Los Angeles. “But we are seeing basically the same response to the global crisis on both continents. IT is part of the solution to weather multiple crises. ”

As always, things could change. There are warning signs of an impending recession or at least a slowdown. And inflation is undoubtedly a factor behind some of the budget increases rather than just the desire to transform. So, the outlook is not all roses and sunshine.

Still, most CIOs are reporting that their budgets are adequate and that companies are asking them to focus more on improving service than on cutting costs.

In other words, IT spending is becoming disconnected from general economic conditions. While some metrics, like employee turnover rate, may be impacted by economic conditions, overall budget growth and most spending priorities do not seem to be affected by poor economic conditions. Growth or recession, IT has a crucial place in the strategy of all enterprises. The question is no longer whether budgets will increase or even by how much. Budgets will increase. And they will increase as needed. The question is how best to deploy these resources to meet the problems of the next few years. The metrics in this study are designed to help you deploy those resources in the best way possible.

This European IT Spending and Staffing Benchmarks study provides IT budgetary benchmarks and IT staffing metrics by industry sector and organizational size for private and public companies and for governmental organizations in Europe, based on our annual, in-depth survey of over 200 information technology executives. The primary goal of this study is to give business and IT leaders in Europe an objective set of industry metrics to understand how their IT spending and staffing levels compare to their industry peers.

This study is a companion study to our main study, which targets organizations with operations in the US and Canada. Comparing the two studies allows us to identify key differences within IT organizations between European organizations and their counterparts in the US and Canada. In the past, we have identified some key differences, including that European companies often outsource more and spend less as a percentage of budget on IT personnel, two likely related numbers. They also tend to have slightly larger IT capital budgets. But what has stood out more than anything about this 2022-2023 study is how similar IT spending is between the two regions. They face many of the same challenges, and they are responding to them in similar ways.

The Computer Economics European IT Spending and Staffing Benchmarks 2022/2023 study is based on a detailed survey of more than 200 IT executives in Europe on their IT spending and staffing plans for 2022/2023. The study provides IT spending and staffing benchmarks for small, midsize, and large organizations and for 14 sectors and subsectors. A description of the study’s metrics, design, demographics, and methodology can be found in the free executive summary.

This Research Byte is a brief overview of the findings in our report, European IT Spending and Staffing Benchmarks 2022/2023. The full 19-chapter report is available at no charge for Avasant Research clients. Individual chapters may be purchased by non-clients directly from our website (click for pricing).