Press Release

Covid Accelerates Digital Disruption And Innovative Business Models In The Insurance Sector

Los Angeles, January, 2021

Changing risk landscapes and worsening loss ratios are shifting the role of insurance companies from risk mitigation to risk prevention. Additionally, the pandemic has put new pressures on business models. Newer risks, evolving customer expectations, and increased competition combined with business continuity challenges have made digital transformation a top priority for insurance carriers. Insurance companies are significantly investing in building digital capabilities to optimize core operations, create nontraditional products, and enhance and personalize the customer experience.

These emerging trends are covered in Avasant’s new Insurance Digital Services 2021-2022 RadarView™ report. The report is a comprehensive study of digital service providers in the insurance space, including top trends, analysis, recommendations, and a close look at the leaders, innovators, disruptors, and challengers in this market.

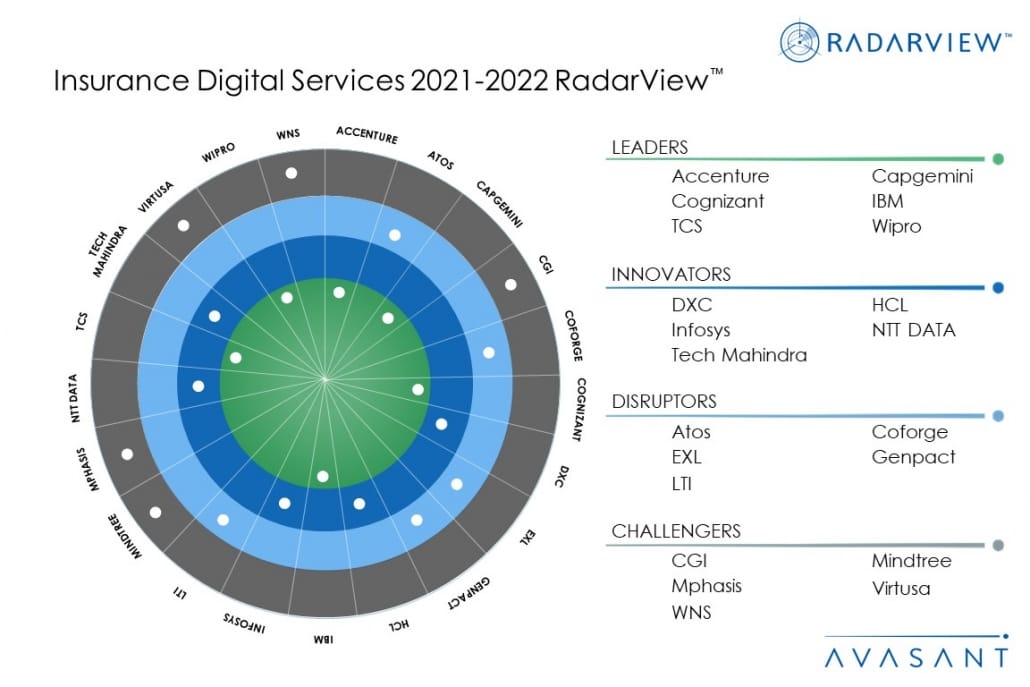

Avasant evaluated 29 providers using three dimensions: practice maturity, investments and innovation, and partner ecosystem. Of those 29 providers, we identified 21 that brought the most value to the market during the past 12 months.

The report recognizes service providers in four categories:

Anupam Govil, a partner and the head of insurance practice with Avasant, congratulated the winners noting, “The pandemic has exacerbated vulnerabilities in traditional insurance business models. Customers expect more personalized solutions that align with their lifestyle and budget. Carriers need to leverage behavioral economics and collaborative ecosystems to compete in the post-COVID economy.”

Some of the findings from the full report include the following:

Property and casualty (P&C) insurance companies should:

Anupam Govil, a partner and the head of insurance practice with Avasant, congratulated the winners noting, “The pandemic has exacerbated vulnerabilities in traditional insurance business models. Customers expect more personalized solutions that align with their lifestyle and budget. Carriers need to leverage behavioral economics and collaborative ecosystems to compete in the post-COVID economy.”

Some of the findings from the full report include the following:

Property and casualty (P&C) insurance companies should:

- Leaders: Accenture, Capgemini,Cognizant, IBM,TCS, and Wipro

- Innovators: DXC, HCL, Infosys, NTT DATA, and Tech Mahindra

- Disruptors: Atos, Coforge, EXL, Genpact, and LTI

- Challengers: CGI, Mindtree, Mphasis, Virtusa, and WNS

Figure 1 from the full report illustrates these categories:

Anupam Govil, a partner and the head of insurance practice with Avasant, congratulated the winners noting, “The pandemic has exacerbated vulnerabilities in traditional insurance business models. Customers expect more personalized solutions that align with their lifestyle and budget. Carriers need to leverage behavioral economics and collaborative ecosystems to compete in the post-COVID economy.”

Some of the findings from the full report include the following:

Property and casualty (P&C) insurance companies should:

- Leverage behavioral economics, IoT,and telematics to develop personalized insurance plans and proactively mitigate risks.

- Use behavior incentivization through telematics and real-time monitoring technologies to offer more flexible and usage-based insurance (UBI) products, especially for auto coverage.

- Create offerings that enable early warning alerts and preventive maintenance due to the industry seeing a gradual shift from risk management to risk prevention. With the expansion of smart home technology and digital touchpoints, insurers need to develop more customized offerings tailored to a customer’s lifestyle and habits.

- Modernize existingchannels,and explore alternate channels for distribution and engagement.

- Acquire new digital capabilities to enable direct customer engagement for P&C insurers heavily dependent on intermediaries. Enable, simultaneously, a more personalized interface with agents and brokers to retain loyalty and maintain a balanced strategy.

- Redesign distribution methods to enable effective digital sales driven by a personalized agent-customer virtual interaction. Build highly-engaged communities that unite people around shared interests and purpose and foster higher brand loyalty.

- Leverage wearables and analytics to manage policyholders’health,and provide personalized value-added services.

- Monitor policyholders’ health and lifestyle by using IoT devices, such as wearables, sensors, and connected medical equipment. Incentivize healthy habits through premium discounts and rewards.

- Prevent or mitigate adverse incidents by predicting risk for disease, mortality, and health status of customers through predictive analytics.

- Reimagine business by accessing and integratinginsurtechcapabilities and harnessing the power of big data.

- Increase the pace of innovation and strengthen existing capabilities by investing in insurtechs focused on three key domains: health monitoring, customer experience, and behavioral/social media analytics.

- Harness the potential of big data from sources such as internet search histories, social media, criminal records and GPS-enabled devices for personalized advertising and promotions, cross-/up-selling, lapsation/attrition control, and fraud prevention.

- Accelerate transition from human-led to AI-led risk modelling and premiums determination

- Scale-up AI adoption for determining optimal pricing policies by performing real-time risk assessments and improving predictions of client damages.

- Develop AI-powered risk modeling techniques in-house or partner with specialized companies like Risk Management Solutions (RMS) or AIR Worldwide (AIR) to ascertain optimal risk premiums.

- Expand reinsurance offerings in emerging risk areas to gain early mover advantage and address nontraditional competition

- Develop and enhance reinsurance product offerings to cover emerging risk areas like cybersecurity, autonomous vehicles, and smart manufacturing (using 3D printing).

- Invest in or partner with start-ups to leverage niche domain expertise in priority areas such as developing cyber-risk models and integrating risk management solutions for auto manufacturers.