Areas of Interest

Content Type

Industries

- Aerospace and defense

- Banking, Financial Services, and Insurance

- Energy and Resources

- Federal Government

- Healthcare and life sciences

- High-tech and telecommunications

- Higher Education

- Media and entertainment

- Private equity

- Public Sector

- Retail and manufacturing

- Social Impact Institutions

- Travel and transportation

Technologies

- Artificial Intelligence

- Automation

- Blockchain

- Business and data analytics

- Cloud

- Customer relationship management (CRM)

- Cybersecurity

- Digital Services

- Enterprise resource planning (ERP)

- Human capital management (HCM)

- Internet Of Things

- Machine Learning

- Networking

- Supply chain management (SCM)

- Virtual reality/Augmented reality

Areas of Interest

Latest Reports

From Seats to Experiences: Reimagining Airline Commerce Through Modern Retailing

As highlighted in the Airlines and Airports Digital Services 2026 Market Insights report, global air passenger traffic continues to scale at an unprecedented pace, driven by rising middle-class populations, expanding international connectivity, and a strong recovery in leisure and business travel demand following the pandemic. In an environment characterized by margin volatility, shifting traveler expectations, and intensifying competition from digital-first travel ecosystems, airlines are increasingly reimagining themselves as modern retailers rather than transportation providers. The focus is rapidly shifting from selling seats to curating personalized, experience-led journeys spanning booking, ancillary services, airport experiences, loyalty ecosystems, and post-trip engagement. Therefore, airlines are modernizing their retailing experience by adopting the New Distribution Capability (NDC) framework introduced by the International Air Transport Association (IATA).

From AI Ambition to Enterprise Execution in APAC: A CIO Playbook

As we all know, the Asia-Pacific (APAC) region has been at the forefront of digital transformation over the past decade. Cloud adoption, mobile-first economies, and platform-led business models have enabled enterprises to scale rapidly and innovate continuously. Hyperscalers such as AWS have played a foundational role in this journey, providing scalable infrastructure, accelerating application modernization, and democratizing access to advanced technologies.

Pax Silica and the Philippines: What the New Economic Security Zone Means for Global Supply Chains

On April 16, 2026, the United States and the Philippines jointly announced plans to establish a 4,000-acre Economic Security Zone within the Luzon Economic Corridor (U.S. Department of State). Designated as the first AI-native industrial acceleration hub under the Pax Silica Initiative, the zone is intended to reduce dependence among partner nations on concentrated supply chains for semiconductors, critical minerals, and advanced manufacturing. With the Philippines formally joining the Pax Silica network alongside countries such as Japan, South Korea, the United Kingdom, and Australia, the announcement signals a meaningful shift in how partner economies are approaching supply chain resilience and economic security in the Indo-Pacific.

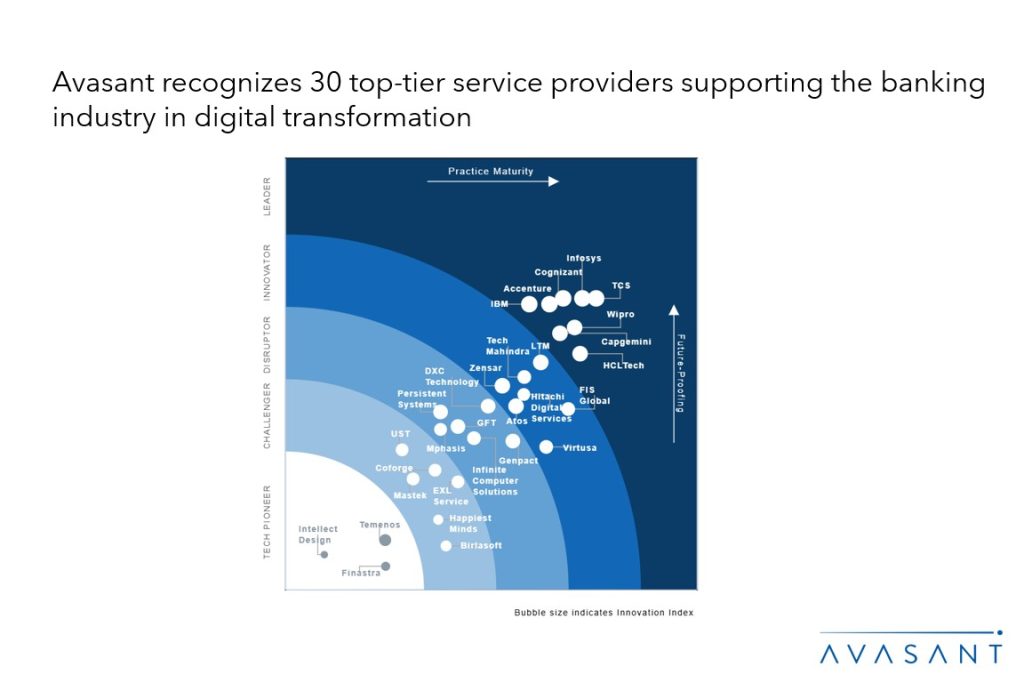

Banking Digital Services 2026 Market Insights™

The Banking Digital Services 2026 Market Insights™ assists organizations in identifying important demand-side trends that are expected to have a long-term impact on any digital project in the banking industry. The report also highlights key challenges that enterprises face today in this space.

Banking Digital Services: Advancing AI‑Native, Resilient, and Customer‑Centric Banking Through Digital Modernization

Banking enterprises are reimagining customer engagement for digitally native consumers, shifting to digital‑first models across the banking life cycle. They are deploying Gen AI and agentic AI across core value streams—from credit memo generation and loan origination to intelligent KYC/AML workflows and real‑time fraud detection. In parallel, banks are investing in real‑time payments enablement and composable orchestration platforms. They are modernizing legacy cores through cloud‑native side‑core and dual‑core architectures. Additionally, banks are embedding compliance‑by‑design into digital platforms, leveraging AI‑driven regulatory intelligence and automated transaction monitoring to strengthen operational resilience.

Banking Digital Services 2026 RadarView™

The Banking Digital Services 2026 RadarView™ helps banking enterprises craft a robust strategy based on industry outlook, best practices, and digital transformation. The report can also aid them in identifying the right partners and service providers to accelerate their digital transformation in this space. The 112-page report also highlights top market trends in the banking space and Avasant’s viewpoint.

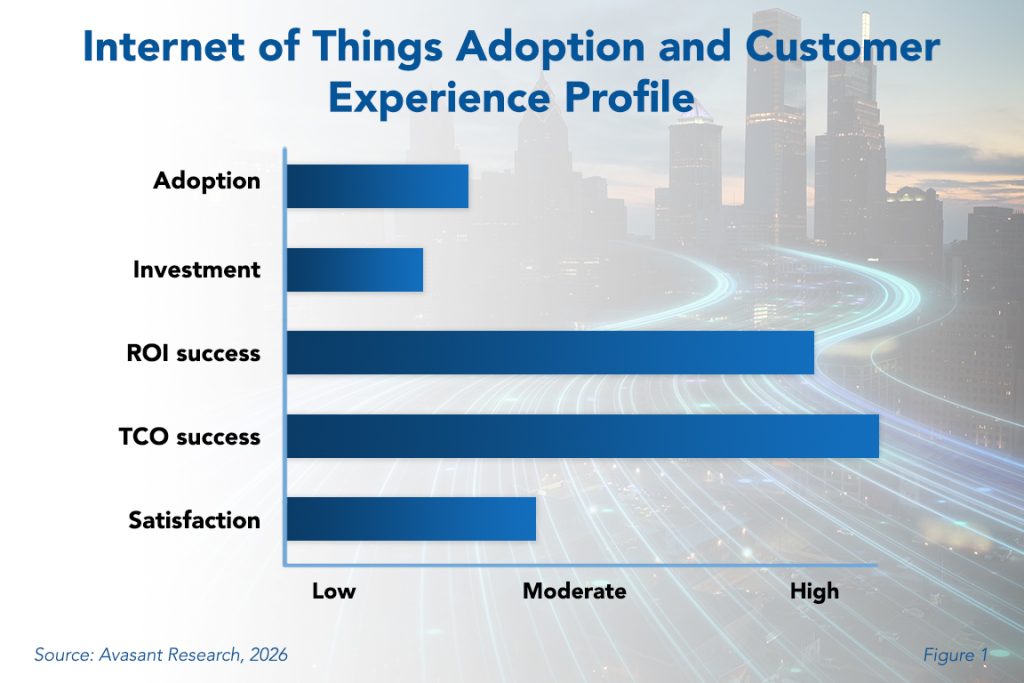

IoT a Success But Complexity Holds Back Investment

While many emerging technologies attract rapid and widespread adoption, the Internet of Things (IoT) follows a markedly different trajectory. Rather than scaling quickly across organizations, IoT adoption remains comparatively limited, reflecting the complexity of implementation, integration challenges, and the specialized use cases it often serves. However, low adoption does not equate to low value. This Research Byte examines the potential causes.

Internet of Things Adoption Trends and Customer Experience 2026

For much of the past decade, the Internet of Things (IoT) struggled to meet enterprise expectations. While cloud computing and artificial intelligence attracted the bulk of capital expenditure, IoT initiatives were often confined to stalled pilots, fragmented standards, and narrowly scoped use cases. As a result, IoT was widely viewed as a technology with promise but limited return. That perception is beginning to shift. The massive investments companies have made in AI are hitting a data ceiling. To evolve from simple chatbots to truly autonomous operations, AI requires the constant, real-world telemetry that only IoT can provide. This “forced maturation” has pushed adoption rates to a historic high of 37%, up from 32% in 2024.

Oracle Cloud ERP Services 2026 Market Insights™

The Oracle Cloud ERP Services 2026 Market Insights™ assists organizations in identifying important demand-side trends that are expected to have a long-term impact on any Oracle Cloud ERP projects. The report also highlights key challenges that enterprises face today.

Oracle Cloud ERP Services: Augmenting ERP Implementations Through Generative AI Solutions

Oracle Cloud ERP modernization is accelerating as enterprises adopt Fusion Cloud SaaS, cloud-native operating models, and phased transformation strategies to standardize processes and improve scalability. Agentic AI adoption is gaining the strongest traction in structured, high-volume functions such as finance and procurement, while industries including telecom, manufacturing, retail, and high-tech are prioritizing AI-enabled use cases to strengthen operational visibility and responsiveness. At the same time, legacy customizations, fragmented processes, and change resistance continue to create implementation risks, increasing the importance of governance maturity, process standardization, and structured change management. Both demand- and supply-side trends are covered in Avasant’s Oracle Cloud ERP Services 2026 Market Insights™ and Oracle Cloud ERP Services 2026 RadarView™, respectively.