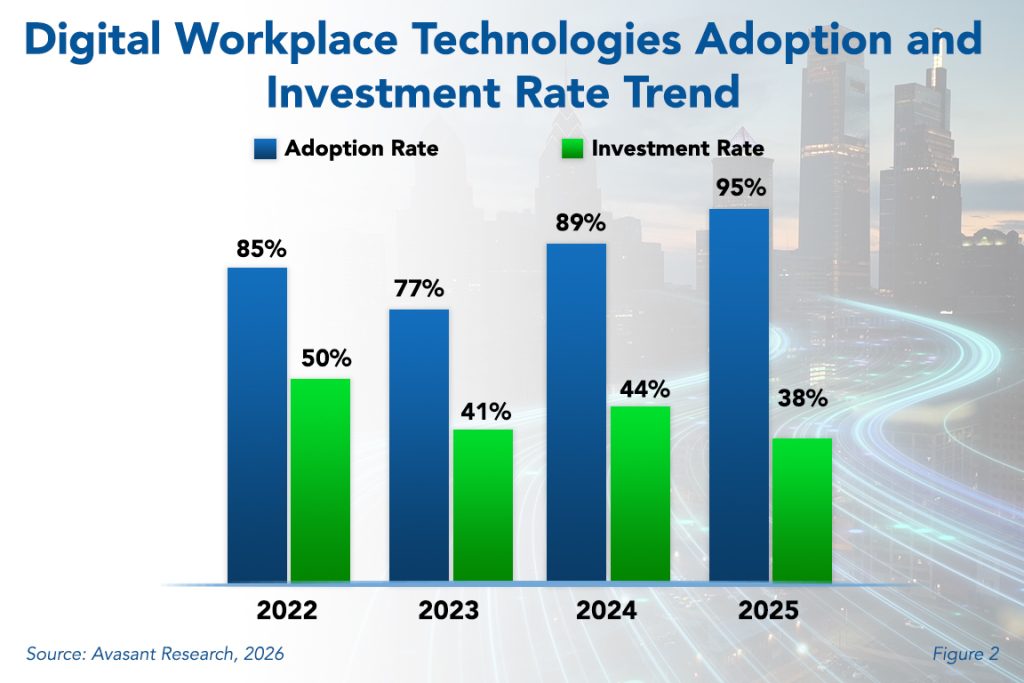

Since 2020, digital workplace technologies have remained central to how organizations operate. These tools have produced measurable gains in efficiency, collaboration, and responsiveness. But as adoption reaches record levels, the focus has shifted from rapid deployment to value realization, ensuring that digital workplace investments are secure, well-governed, and aligned to how employees actually work. This Research Byte summarizes our full report, Digital Workplace Technologies Adoption and Customer Experience.

Digital workplace technologies have moved from being an enabler of remote work to a foundational layer of enterprise operations. Today, they allow employees to communicate, collaborate, and access critical applications securely from anywhere, integrating a broad set of tools into a unified digital environment. Since 2020, these technologies have remained central to how organizations operate, driving measurable gains in efficiency, collaboration, and responsiveness. As adoption reaches record levels, the focus has shifted from rapid deployment to value realization, ensuring that digital workplace investments are secure, well-governed, and aligned to how employees actually work. Well‑defined desktop personas and robust security practices are therefore no longer optional, but essential to sustaining performance at scale.

Our quarterly Residual Value Forecast (RVF) report provides forecasts for the following categories of IT equipment: desktop computers, laptops, network equipment, printers, servers, storage devices, and other IT equipment. It also includes residual values for other non-IT equipment in the following categories: copiers, material handling equipment (forklifts), mail equipment, medical equipment, test equipment, and miscellaneous equipment such as manufacturing machinery and NC machines. Residual Value Forecasts are provided for five years for end-user, wholesale, and orderly liquidation values (OLV) prices.

Enterprise AI investment is accelerating, but most organizations remain far from true autonomy. This article argues that the gap between AI spending and autonomous outcomes is not caused by model capability, but by how enterprises define value, govern data, measure performance, structure human oversight, prepare the workforce, and contract for delivery. Drawing on insights from senior leaders at Hertz, IBM, IFF, and Prudential at Avasant’s Empowering Beyond Summit 2026, it identifies six barriers that repeatedly stall progress. It also introduces practical lenses such as Proof of Value, data trust, and decision-based operating models to explain what differentiates scalable autonomy from disconnected experimentation. The article closes with a practitioner playbook that translates those lessons into operational actions for enterprise leaders.

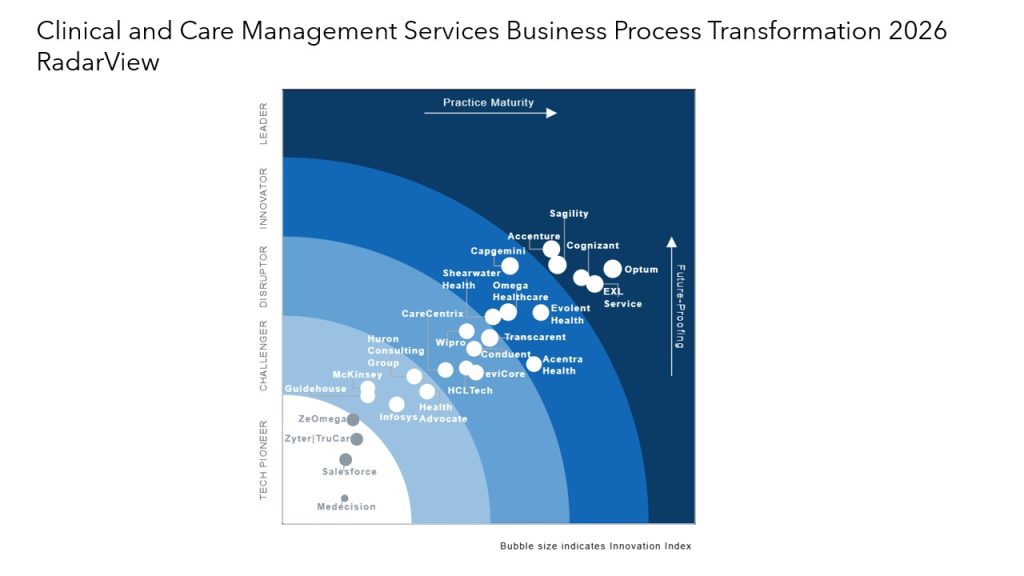

The Clinical and Care Management Services Business Process Transformation 2026 Market Insights™ provides a detailed view of enterprise demand-side trends shaping clinical operations and care management. It highlights how organizations are restructuring workflows, adopting AI-enabled systems, and transitioning toward longitudinal care models to manage cost, complexity, and scalability.

Clinical and care management is transitioning from fragmented, labor-intensive workflows to AI-enabled, platform-led operating models that orchestrate continuous, longitudinal care. Enterprises and payors are embedding generative AI, automation, interoperability, and workflow orchestration into utilization management, case management, appeals, and population health processes to improve throughput, consistency, and clinical outcomes. These models enable earlier risk identification, faster decision-making, and reduced administrative burden by automating intake, evidence extraction, documentation, and routing before clinical intervention. However, this transformation introduces new challenges, including regulatory constraints, AI governance requirements, workforce reconfiguration, and integration complexity across legacy systems. Despite these constraints, clinical and care management is evolving into an intelligence-driven, outcome-oriented model, where success depends on the ability to scale AI within governed workflows while maintaining clinical oversight and care quality.

The Clinical and Care Management Services Business Process Transformation 2026 RadarView™ provides insights to help organizations redesign clinical and care management operations and build scalable, technology-enabled care delivery models. It identifies leading service providers supporting this transformation and evaluates their capabilities across clinical workflows, technology integration, and delivery execution. The report includes detailed provider profiles, comparative analysis, and Avasant’s perspective on emerging trends shaping the market.

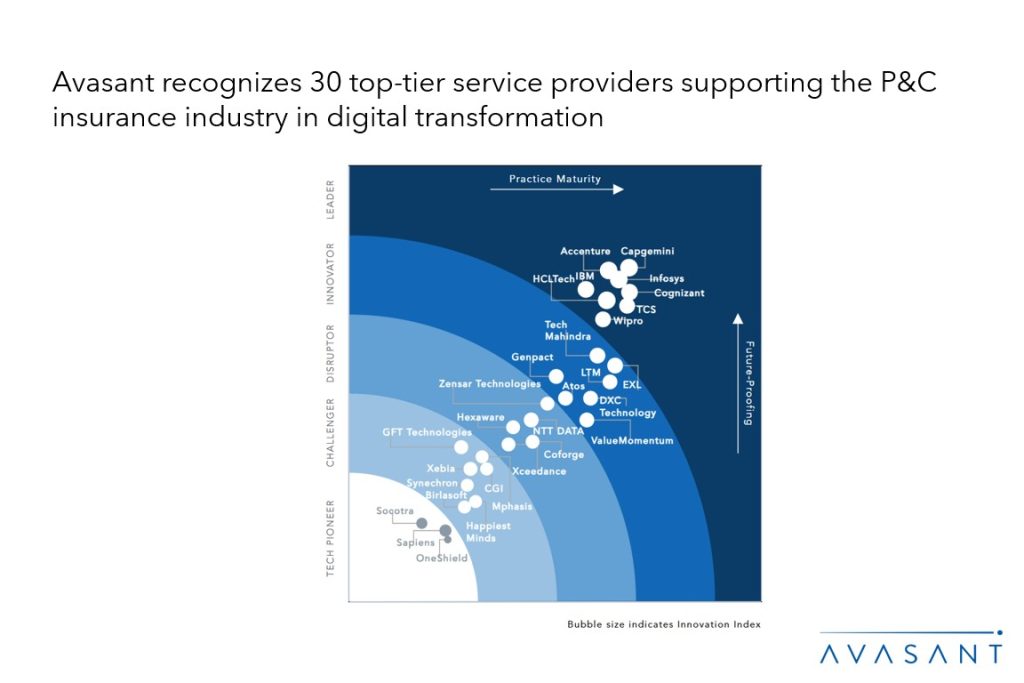

The Property and Casualty Insurance Digital Services 2026 Market Insights™ assists organizations in identifying important demand-side trends that are expected to have a long-term impact on any digital project in the P&C insurance industry. The report also highlights key challenges that enterprises face today in this space.

As the property and casualty (P&C) insurance industry continues to move toward an AI-native era, it confronts various market challenges, including escalating climate volatility and secondary perils, sustained cost pressures eroding margins, and policyholders demanding tailored coverage and real-time service. Insurers are embedding generative AI and agentic AI across underwriting, claims, and policyholder engagement to orchestrate end-to-end workflows and reposition global capability centers as judgment-led engineering hubs. Dynamic risk engines fueled by geospatial intelligence, IoT, and telematics are enabling property-level pricing and continuous exposure monitoring, while intermediary platforms deliver instant appetite clarity and AI-powered decision support to agents, brokers, and managing general agents. To navigate this shift, enterprises should partner with service providers to scale agentic AI, real-time risk analytics, and intermediary enablement for resilient, AI-led growth.

The Property and Casualty Insurance Digital Services 2026 RadarView™ can help enterprises craft a robust strategy based on industry outlook, best practices, and digital transformation. The report can also aid them in identifying the right partners and service providers to accelerate their digital transformation. The 110-page report also highlights top supply-side trends in the P&C insurance digital services space and Avasant’s viewpoint.

Login to get free content each month and build your personal library at Avasant.com