The growing enterprise demand for multisourcing service integration (MSI) is mainly driven by complexities in multivendor environments and the need for optimizing IT costs and enhancing service outcomes and quality. Service providers offer multiple end-to-end services to help organizations streamline service delivery processes, enhance supplier management, mitigate risks, and improve vendor collaboration. Additionally, service providers invest in advanced technologies such as AI/ML, automation, and proprietary IT service management tools to optimize service delivery and improve overall outcomes. This rising demand for MSI has also led to a 46% increase in the number of full-time employees working in this field.

Both demand-side and supply-side trends are covered in our Multisourcing Service Integration 2022–2023 Market Insights™ and Multisourcing Service Integration 2022–2023 RadarView™ , respectively. These reports present a comprehensive study of MSI service providers and closely examine market leaders, innovators, disruptors, and challengers.

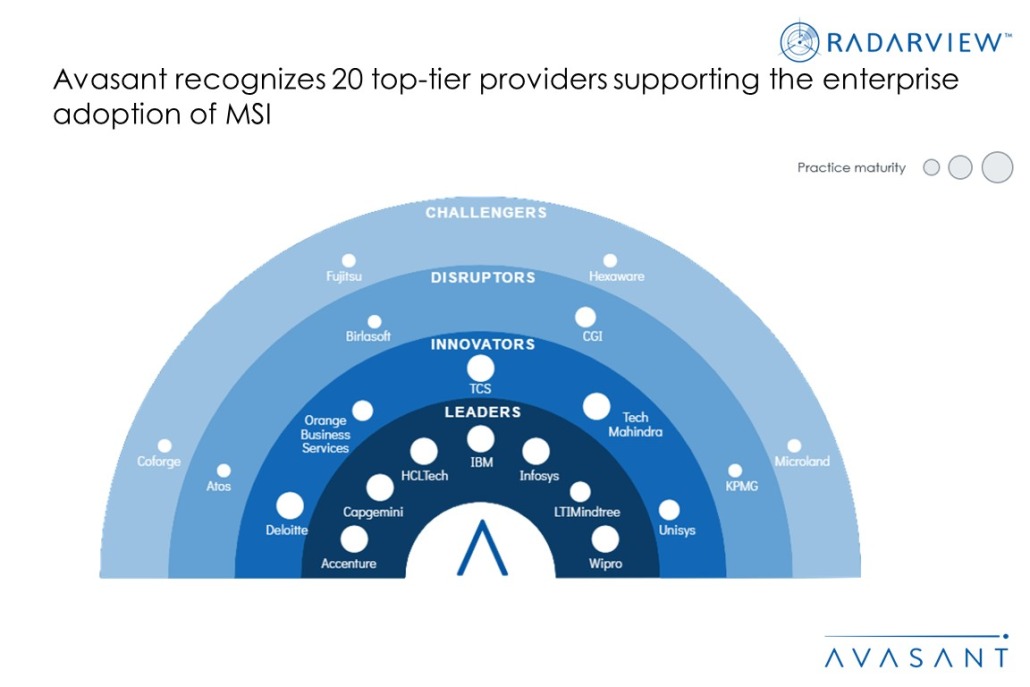

We evaluated 32 service providers across three dimensions: practice maturity, partner ecosystem, and investments and innovation. Of the 32 providers, we recognized 20 that brought the most value to the market during the past 12 months.

The report recognizes service providers in four categories:

Figure 1 below from the full report illustrates these categories:

“The success of MSI lies in its ability to provide a unified view of service delivery processes,” said Avasant Principal James Lee. “This approach allows organizations to make informed decisions and optimize their overall service delivery performance.”

The reports provide several findings, including the following:

“Enterprises seek value in MSI to improve overall business agility,” said A. Tarun, senior research analyst with Avasant. “By streamlining service delivery processes and optimizing supplier relationships, organizations can better manage risks and respond more quickly to changing market conditions.”

The report also features detailed RadarView profiles of 20 service providers, along with their solutions, offerings, and experience in assisting enterprises in their MSI journeys.

This Research Byte is a brief overview of the Multisourcing Service Integration 2022–2023 Market Insights™ and Multisourcing Service Integration 2022–2023 RadarView™. (click for pricing).