Areas of Interest

Content Type

Industries

- Aerospace and defense

- Banking, Financial Services, and Insurance

- Energy and Resources

- Federal Government

- Healthcare and life sciences

- High-tech and telecommunications

- Higher Education

- Media and entertainment

- Private equity

- Public Sector

- Retail and manufacturing

- Social Impact Institutions

- Travel and transportation

Technologies

- Artificial Intelligence

- Automation

- Blockchain

- Business and data analytics

- Cloud

- Customer relationship management (CRM)

- Cybersecurity

- Digital Services

- Enterprise resource planning (ERP)

- Human capital management (HCM)

- Internet Of Things

- Machine Learning

- Networking

- Supply chain management (SCM)

- Virtual reality/Augmented reality

Areas of Interest

Latest Reports

Digitization to Improve Patient Convenience and Drive Profitability

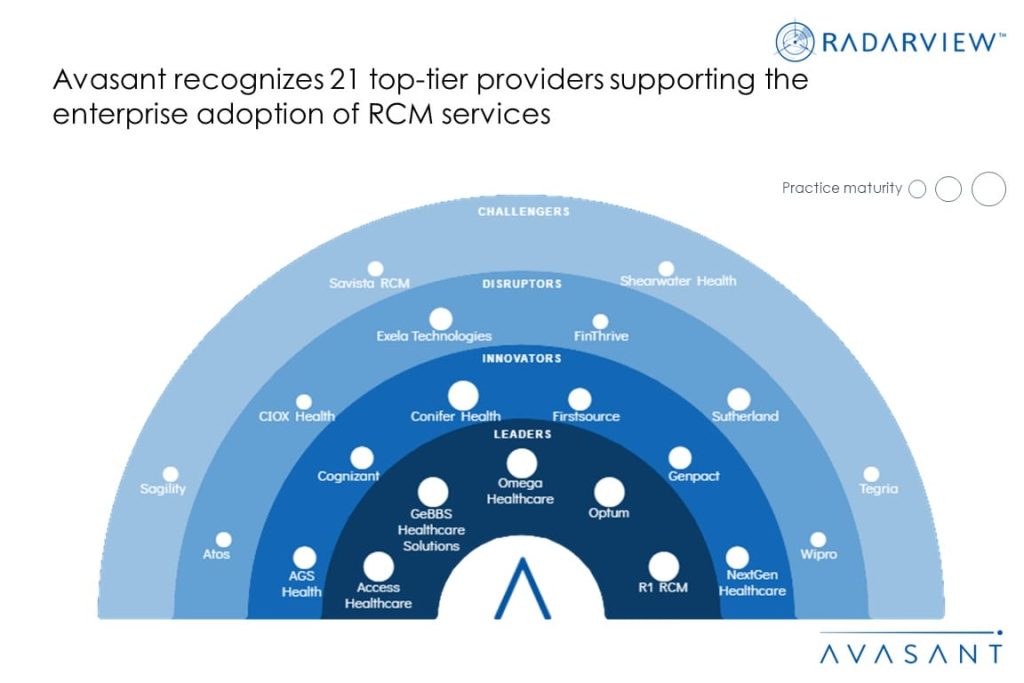

Rising healthcare and operational costs pose a challenge to improving patient experience, collections, and provider margins, making them vulnerable to recession. Though physician and provider productivity is increasing as patients continue to reengage and seek care that was put off during the pandemic, there was a 12% YOY increase in median investment/subsidy per provider FTE. Healthcare providers also need to address patients expecting seamless digital interactions, desiring convenience and empowerment in their care journey to improve their experience. In order to support these, they increasingly rely on revenue cycle management (RCM) service providers’ expertise through outsourcing. This is evident from a 15%–25% increase in the revenue of RCM outsourcing service providers in 2021–2022. Both demand-side and supply-side trends are covered in our RCM Business Process Transformation 2023 Market Insights™ and RCM Business Process Transformation 2023 RadarView™, respectively.

RCM Business Process Transformation 2023 Market Insights™

The RCM Business Process Transformation 2023 Market Insights™ assists organizations in identifying important demand-side trends that are expected to have a long-term impact on any RCM services project. The report also highlights key challenges that enterprises face today.

RCM Business Process Transformation 2023 RadarView™

The RCM Business Process Transformation 2023 RadarView™ assists organizations in identifying strategic partners for RCM services by offering detailed capability and experience analyses of service providers in this space. It provides a 360-degree view of the service providers across practice maturity, domain ecosystem, and investments and innovation, thereby supporting enterprises in identifying the right RCM services partner. The 66-page report highlights top supply-side trends in the RCM services space and Avasant’s viewpoint.

High-Tech Industry: Driving Innovation in High-Tech through Digital Transformation

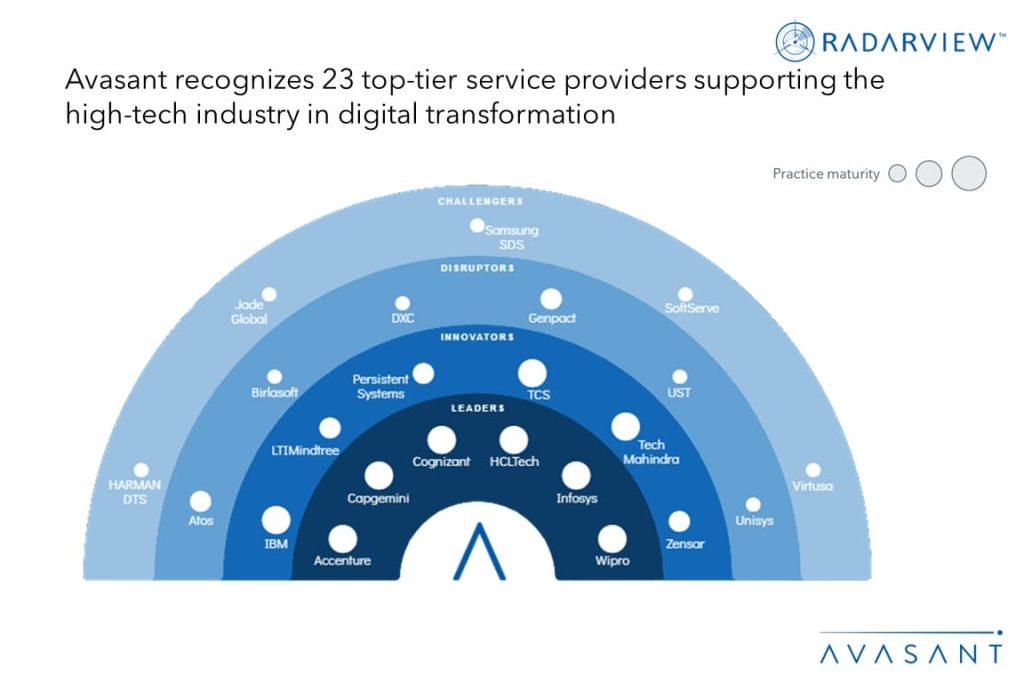

The High-Tech Industry Digital Services 2023–2024 RadarView™ can help high-tech enterprises craft a robust strategy based on industry outlook, best practices, and digital transformation. The report can also aid them in identifying the right partners and service providers to accelerate their digital transformation in this space. The 89-page report also highlights top market trends in the high-tech industry and Avasant’s viewpoint.

High-Tech Industry Digital Services 2023–2024 Market Insights™

The High-Tech Industry Digital Services 2023–2024 Market Insights™ assists organizations in identifying important demand-side trends that are expected to have a long-term impact on any digital projects in the high-tech industry. The report also highlights key challenges that enterprises face today.

High-Tech Industry Digital Services 2023–2024 RadarView™

The High-Tech Industry Digital Services 2023–2024 RadarView™ can help high-tech enterprises craft a robust strategy based on industry outlook, best practices, and digital transformation. The report can also aid them in identifying the right partners and service providers to accelerate their digital transformation in this space. The 89-page report also highlights top market trends in the high-tech industry and Avasant’s viewpoint.

Fostering Sustainability in the Supply Chain by Leveraging Digital Platforms

This article sheds light on how enterprises are increasing their reliance on digital platforms and IT for their supply chain management processes to drive green and sustainable practices across the three levels: supplier, organizational, and distribution. By harnessing the power of IT, businesses are gaining the ability to track, analyze, and optimize their supply chains, resulting in reduced environmental impact, improved social responsibility, and enhanced overall sustainability.

Data Management and Analytics Spike Likely Unsustainable

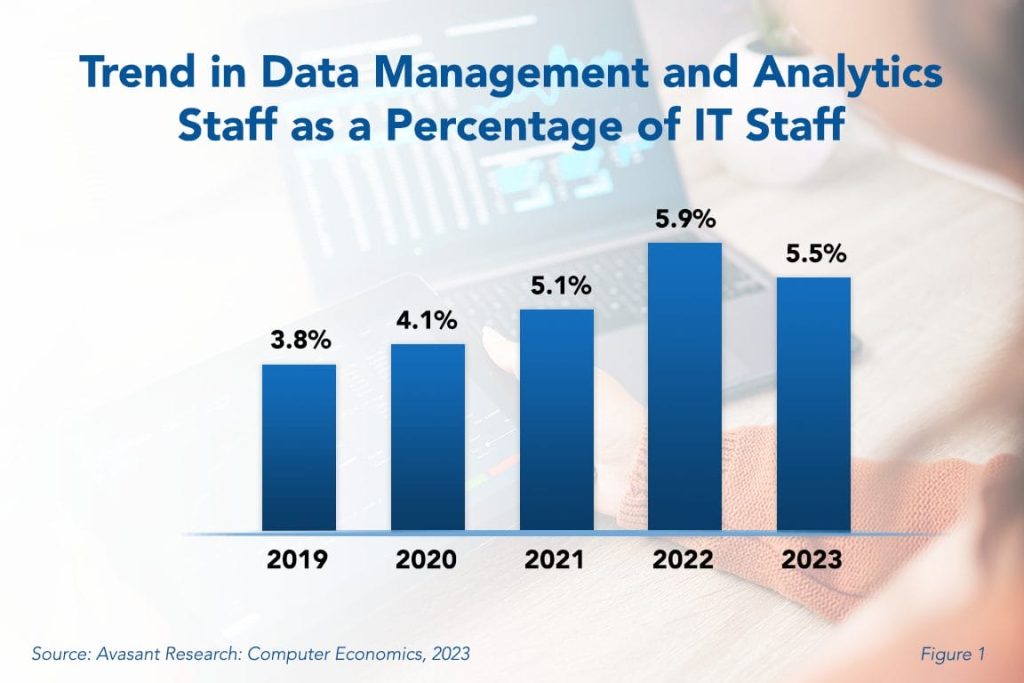

With the amount of data that IT organizations need to manage growing with no end in sight, it is surprising that the data management and analytics function has decreased this year. This Research Byte examines the reasons for the declining trend and provides a summary of our full report on data management staffing ratios.

Data Management and Analytics Staffing Ratios 2023

The amount of data that IT organizations need to manage is growing with no end in sight. Whether it be sensor data from IoT devices, social networking data, online advertising and e-commerce transactions, or multimedia files, the complexity of the data to be analyzed also is increasing. With the continued growth of data and its importance in the day-to-day activities of organizations, it is surprising that the data management and analytics function has decreased this year. After significant growth over previous years, this staffing ratio has declined to 5.5% in 2023 from 5.9% in 2022.

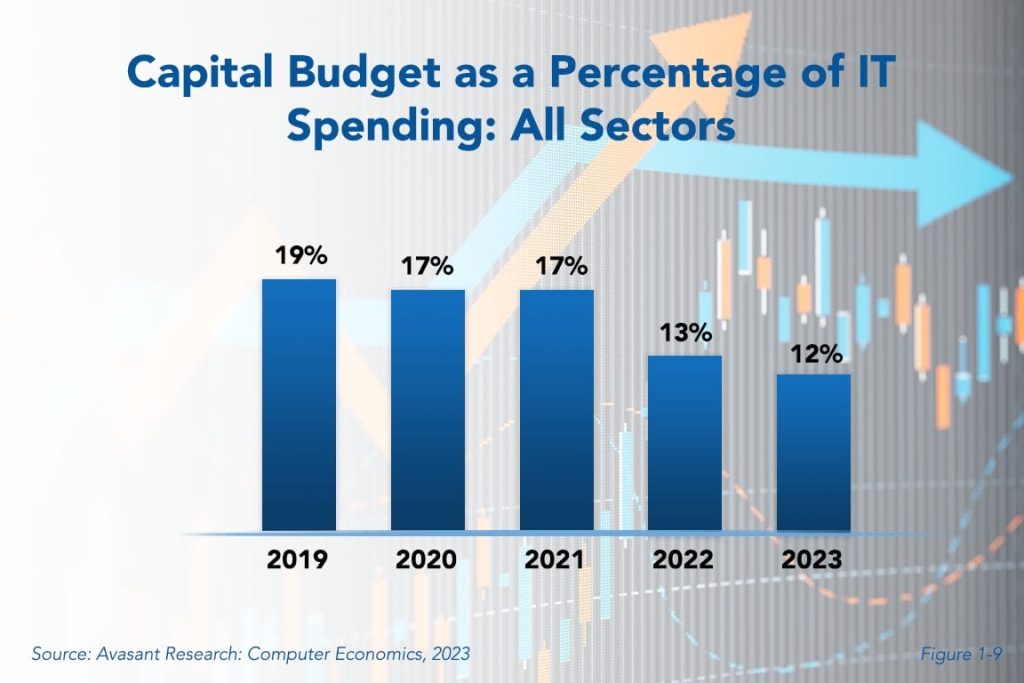

How Low Can They Go? IT Capital Budgets Still Declining

It is not a surprise that capital budgets are falling as a percentage of total IT budgets. Cloud and SaaS have been diverting capital spending for quite some time. But what is a surprise is that capital spending continues to fall even though it only makes up 12% of the total IT budgets. IT capital spending will never disappear completely, but just where is the floor? This research byte is a brief description of some of the findings in our IT Spending and Staffing Benchmarks 2023/2024 study.